India’s AI startup ecosystem is expanding at extraordinary speed. Since the launch of generative AI models such as OpenAI’s GPT series and the rapid adoption of enterprise copilots, hundreds of Indian founders have entered the market promising AI-powered automation for sales, customer support, legal workflows, coding, healthcare documentation, HR operations, and finance.

On the surface, the momentum appears strong. India has one of the world’s largest developer populations, rapidly growing SaaS expertise, improving digital infrastructure, and a large enterprise market increasingly willing to experiment with AI tools.

Yet beneath the excitement lies a structural problem many investors and founders are now openly discussing: a significant portion of Indian AI startups may never become independent platforms or enduring software companies. Instead, many risk becoming temporary “features” that global technology platforms can absorb, replicate, or bundle into larger ecosystems.

This is not merely a startup execution issue. It is increasingly becoming an economic and infrastructure problem.

The next phase of India’s AI ecosystem may depend less on who can launch fastest and more on who can build defensible value beyond foundational models controlled by a handful of global companies.

The Rise of India’s AI Startup Wave

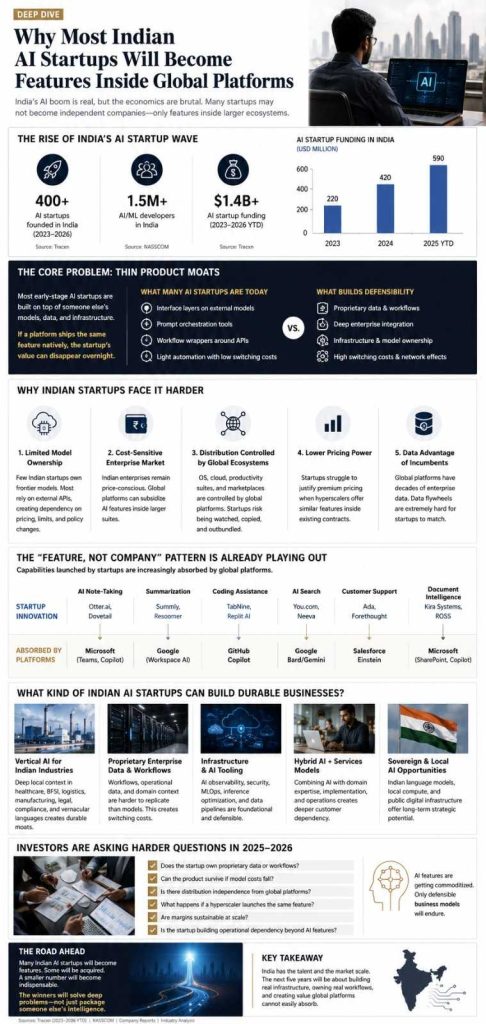

India’s AI startup surge accelerated sharply between 2023 and 2026. Much of this growth was driven by three overlapping trends:

- widespread enterprise experimentation with generative AI

- falling barriers to software development using APIs

- increased investor appetite for AI-native SaaS products

Many startups were able to build minimum viable products quickly using APIs from companies such as OpenAI, Anthropic, Google, and Meta.

This dramatically reduced development complexity. Small teams could launch AI copilots, workflow assistants, or document automation products within weeks rather than years.

For India’s startup ecosystem, this created a familiar pattern reminiscent of earlier SaaS booms:

- rapid product launches

- aggressive AI positioning

- enterprise pilots

- investor-led growth narratives

- crowded categories with limited differentiation

But unlike traditional SaaS, generative AI products are heavily dependent on external model providers.

That dependence changes the economics.

The Core Problem: Thin Product Moats

Historically, successful software companies built defensibility through:

- proprietary infrastructure

- unique distribution

- network effects

- switching costs

- exclusive datasets

- deep workflow integration

Many early-stage AI startups today possess few of these advantages.

Instead, a large number are essentially:

- interface layers on top of foundational models

- workflow wrappers around APIs

- prompt orchestration tools

- lightweight automation systems

This creates a dangerous vulnerability.

If a global platform provider introduces the same capability natively, the startup’s value proposition can collapse quickly.

The pattern has already emerged globally.

Features initially launched by startups in:

- AI note-taking

- summarization

- transcription

- coding assistance

- customer support automation

- AI search

- document intelligence

have increasingly been integrated directly into larger ecosystems from companies such as Microsoft, Google, Notion Labs, Salesforce, and Adobe.

In many cases, the platform advantage is overwhelming:

- existing enterprise distribution

- integrated productivity ecosystems

- massive compute infrastructure

- direct access to proprietary user data

- lower marginal pricing power

For startups competing solely on AI features, survival becomes difficult.

Why Indian Startups Face a Harder Version of the Problem

Indian AI startups face the same platform risks as global startups, but several local structural realities make the challenge more severe.

1. Limited Foundational Model Ownership

Very few Indian companies control large-scale frontier AI models.

Training advanced large language models requires:

- enormous GPU infrastructure

- high-quality multilingual datasets

- massive capital expenditure

- long-term research investment

Most Indian startups instead rely on external APIs.

This creates dependency on:

- pricing decisions

- rate limits

- model policy changes

- latency issues

- platform restrictions

When the core intelligence layer belongs to another company, long-term strategic control weakens significantly.

2. Enterprise AI Spending in India Remains Cost Sensitive

Indian enterprises are adopting AI, but spending patterns remain cautious compared to North America.

Many CIOs and enterprise buyers still prioritize:

- automation ROI

- operational savings

- workflow efficiency

- low implementation costs

This often pressures startups into pricing aggressively.

Meanwhile, global platforms can subsidize AI features across broader enterprise software suites.

For example:

- AI copilots bundled into productivity subscriptions

- AI assistants integrated into CRM platforms

- AI workflow automation included inside existing contracts

Standalone startups then struggle to justify premium pricing.

3. Distribution Is Increasingly Controlled by Global Ecosystems

Distribution is becoming one of the largest bottlenecks in AI.

A technically strong product no longer guarantees sustainable growth.

Global platforms already control:

- operating systems

- cloud infrastructure

- productivity tools

- enterprise collaboration platforms

- developer ecosystems

- app marketplaces

Indian startups often rely on these ecosystems for customer acquisition.

This creates a structural imbalance:

the platform owner can observe market demand patterns and eventually launch competing native features.

The “Feature, Not Company” Debate Is Becoming More Relevant

The phrase “feature, not a company” has existed in Silicon Valley for years, but generative AI has intensified the debate dramatically.

The reason is simple:

AI dramatically lowers the cost of adding new features to existing platforms.

A large SaaS company can now integrate:

- summarization

- search

- chat interfaces

- document generation

- workflow automation

- voice interaction

far faster than before.

This compresses the innovation window for startups.

In earlier software cycles, startups sometimes had years to establish dominance before incumbents reacted.

In AI, that window may shrink to months.

Indian AI Startups That Could Still Build Durable Businesses

Despite the risks, the conclusion is not that Indian AI startups are doomed.

The more important distinction is between:

- AI wrappers

and - AI-native systems with durable advantages

The startups most likely to survive are building deeper operational value.

Areas With Better Defensibility

Vertical AI for Indian Industries

Startups solving deeply localized problems may retain stronger moats.

Examples include:

- Indian healthcare documentation workflows

- vernacular language AI systems

- compliance automation for Indian regulations

- logistics optimization

- manufacturing intelligence

- BFSI workflow automation

Localized domain expertise is harder for global platforms to replicate quickly.

Proprietary Enterprise Data Systems

AI models alone are increasingly commoditized.

But proprietary enterprise workflows and datasets are not.

Startups embedded deeply inside customer operations gain:

- switching costs

- workflow dependency

- operational context

- custom fine-tuning opportunities

This resembles the evolution of earlier enterprise SaaS businesses.

Infrastructure and AI Tooling

Some investors believe India’s strongest long-term AI opportunity may lie in infrastructure rather than consumer AI applications.

This includes:

- AI observability

- data pipelines

- AI security

- inference optimization

- multilingual model tooling

- enterprise deployment systems

These layers are often less vulnerable to rapid feature commoditization.

The Open-Source Shift Could Change the Equation

Open-source AI models may partially reduce platform dependency over time.

Models from organizations such as Meta and emerging open-source ecosystems have lowered entry barriers for startups seeking more control over deployment and customization.

However, open-source does not eliminate infrastructure challenges.

Serving large-scale AI systems still requires:

- GPUs

- inference optimization

- engineering expertise

- cloud spending

- security infrastructure

This means the economic advantage still favors larger players.

India’s Talent Advantage Is Real — But Commercialization Remains Difficult

India undeniably possesses strong AI engineering talent.

Major global AI firms continue expanding engineering and research operations across cities including:

- Bengaluru

- Hyderabad

- Pune

- Chennai

Indian-origin researchers and engineers are also deeply represented in global AI companies.

The challenge is not talent scarcity.

The challenge is converting technical capability into globally defensible AI businesses.

Historically, India excelled in:

- IT services

- implementation

- engineering execution

- cost-efficient software delivery

But platform creation at global scale requires:

- original research

- patient capital

- infrastructure ownership

- distribution power

- long-term ecosystem building

These remain harder to build.

Investors Are Becoming More Selective

Between 2023 and 2024, many AI startups received attention simply for integrating generative AI features.

By 2025 and 2026, investor scrutiny has become sharper.

Many venture firms now increasingly ask:

- Does the startup own proprietary data?

- Can the product survive if model costs fall?

- Is there distribution independence?

- What happens if a hyperscaler launches the same feature?

- Are margins sustainable?

- Is the startup building workflow dependency?

This shift mirrors earlier SaaS market corrections where superficial differentiation struggled to survive.

The Real Opportunity May Be Hybrid AI Businesses

Some analysts believe the strongest Indian AI companies may not resemble pure software startups at all.

Instead, successful firms could combine:

- AI infrastructure

- domain expertise

- enterprise services

- workflow integration

- industry specialization

This hybrid approach aligns more closely with India’s historical strengths.

Rather than competing directly against global frontier model companies, Indian firms may succeed by becoming indispensable operational intelligence partners for enterprises.

Sovereign AI Ambitions Are Growing, But Challenges Remain

India has also increased focus on sovereign AI infrastructure and domestic model development.

Government-backed initiatives and semiconductor ambitions are gaining momentum, particularly around:

- local compute infrastructure

- Indian language AI

- public digital infrastructure

- strategic AI independence

However, building globally competitive foundational AI ecosystems requires sustained long-term investment.

The gap between:

- application-layer startups

and - foundational AI infrastructure companies

remains substantial.

The Future of Indian AI Startups Will Depend on One Question

The defining question for Indian AI startups over the next five years may be:

“Are they solving a deep operational problem, or merely packaging access to someone else’s intelligence layer?”

That distinction will likely determine:

- pricing power

- survival

- acquisition outcomes

- long-term independence

Many startups launched during the generative AI boom may eventually disappear into larger ecosystems.

Some will be acquired.

Others will become integrations inside enterprise suites.

A smaller number may evolve into durable companies with defensible infrastructure, proprietary workflows, and strong enterprise relationships.

Those companies will likely define India’s real AI success stories.

Conclusion

India’s AI startup ecosystem is entering a more mature and difficult phase.

The initial excitement around generative AI dramatically lowered product creation barriers, but it also accelerated commoditization. In this environment, simply building AI-enabled software is unlikely to create lasting value.

Global technology platforms possess overwhelming advantages in:

- infrastructure

- distribution

- compute access

- enterprise reach

- integrated ecosystems

That reality means many Indian AI startups risk becoming temporary features rather than enduring businesses.

But the outlook is not pessimistic — it is selective.

The startups that survive are more likely to be those that:

- solve domain-specific problems

- own proprietary workflows

- embed deeply into enterprise operations

- build infrastructure advantages

- create operational dependency beyond AI features alone

India has the engineering talent and market scale to produce important AI companies. The challenge now is whether those companies can move beyond interface-layer innovation and build defensible systems that global platforms cannot easily absorb.

Also Read : The Rise of “Zombie Startups” in India: Venture-Funded Companies That Stopped Growing but Refuse to Die

Add Startup Magazine as a preferred source on Google-Click Here

Last Updated on Wednesday, May 20, 2026 4:37 pm by Startup Magazine Team